Ironically — accepting payments costs money. If you want to get paid for your services, you must accept various payment methods, such as traditional credit cards, digital wallets, or even cryptocurrency. And in most cases, it's not you as a merchant moving the money between the bank accounts. So, where’re your funds at?

Each transaction consists of multiple players including banks and credit card networks validating the data and passing answers to each other. The merchant sees only two end-points: the cardholder sending the money, and the funds appearing in your merchant account. Everything that happens in between is called payment processing.

Here we’ll discuss how payment processing works and who takes care of transactions. Specifically, we’ll look at credit card processing and credit card networks from the perspective of a payment service provider for merchants.

How payment processing works

Every type of sale entails moving money from the buyer's bank account to the merchant’s bank account. Easy as it is – just a money transfer between the two banks, right? However, as we deal with sensitive data (card ID, transaction amount), multiple companies are involved in validating the information. Secondly, we also need to notify every participant about the transaction.

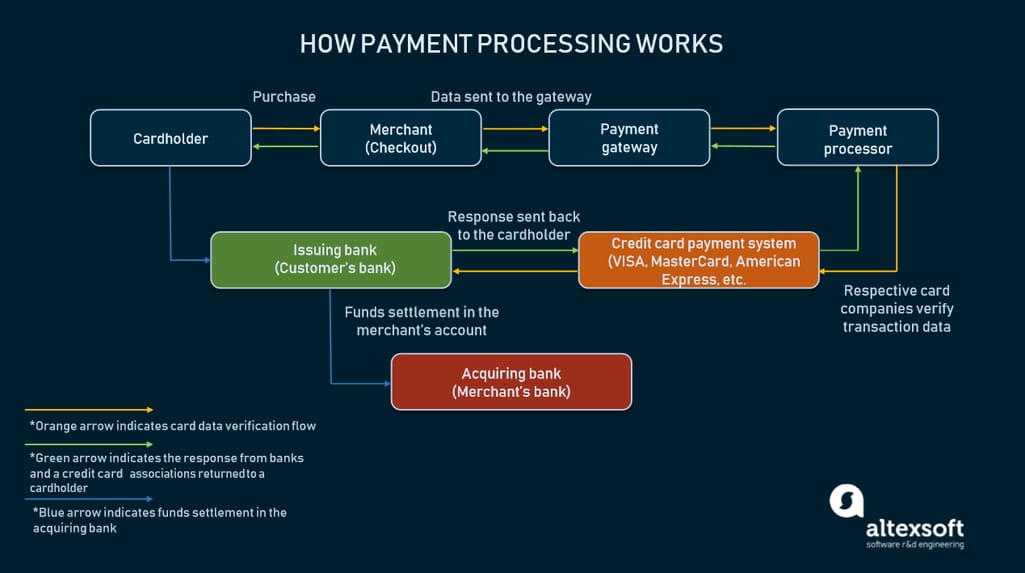

Payment processing flow

The whole cycle of these actions, validations, interchanges, and the actual money transfer is what we call payment processing. Now, from the merchant’s standpoint, processing is a service of several entities. And each of them charges its fee based on transaction parameters. To understand how the process looks from the inside, we’ll break it down by the main participants at every stage of a cycle:

Payment processing in a nutshell

A cardholder. The cardholder (customer) enters their credit card data on the merchant’s payment page. This may involve additional steps like 3D secure check.

A merchant. In the case of an online business, merchants receive transactional data through a specific type of security technology, a payment gateway. At this stage, the merchant sees only the transaction amounts, and here begins the actual processing.

A payment gateway. Think of a payment gateway as the digital equivalent of physical terminals in brick and mortar stores. The gateway encrypts the information, passes it to the corresponding payment processor, and charges a fee for data transition.

A payment processor. After the transactional data is sent through a gateway, it gets to the payment processor. This is a company that validates all the data and asks participants for a money transfer. The payment processor

fetches encrypted data from a payment gateway. A fee is charged.

asks the issuing (cardholder’s) bank if there is enough money to make a purchase. A fee is charged and paid to the issuing bank.

receives the answer. The transaction is approved or denied.

sends transaction data to a credit card network for validation. A fee is charged and paid to the network.

receives the answer. The transaction is approved or denied.

informs the customer about the successful transaction or denial. This is done through a bank.

initiates a money transfer between the issuing bank (customer’s bank account) and the acquiring bank (merchant’s account). A fee is charged.

A credit card network. Credit card networks act as validators of credit cards of their brand. It means that whenever a payment made with MasterCard comes into processing, MasterCard will validate each card. A fee is also charged.

An issuing bank. After all the validation layers are passed, the issuing bank would receive transaction data and initiate the money transfer to the acquiring bank. Simultaneously, it lets the cardholder know about the funds charged to their account.

Merchant-wise, payment processing is a service, handled by different companies, each covering their chunk of the process. Additionally, every participant takes its fee.

Payment processing fees

For the merchant, there are three types of fees that constitute the general processing cost.

Interchange fee. Usually, an interchange fee is what the customer’s card issuing bank receives for a transaction. Credit card networks set the amount of these fees. The interchange is generally a sum of money calculated of all operations between the processing participants. The interchange fee covers the expenses for data transfer and money transfer and can be split between processing participants.

Assessment fee. Assessment fees go to credit card networks. the amount depends on the card type (credit or debit), transaction location (international or domestic), and other factors.

Markup can be thought of as any additional fees included in the transaction. However, the markup is always hidden, because it’s inconsistent and is invoked whenever there are transaction cancellations, refunds, or additional processing fees. This is a sum of money split between all the payment processing participants to cover expenses. As markup fees are inconsistent, we won’t cover them in detail here.

Credit card networks and payment processors

As we deal mostly with credit cards, our major payment method, we should know about the place of credit card networks in processing.

A credit card network is in charge of regulating credit card processing and usage terms. The four major networks are Visa, MasterCard, American Express, and Discover. Banks that issue the cards by brand names of these networks are called credit card companies. Some networks like Discover and American Express (Amex) issue cards on their own, as they are banks as well. Visa and MasterCard are more of a brand, letting partnered banks distribute their cards.

In processing terms, credit card networks are the regulators that define fees and standards. Any time a Visa or MasterCard (networks) card issued by Capital One or Crédit Agricole (banks) is involved in the payment, the network would process and validate some part of the transaction and charge a fee.

A payment processor can be a technological or financial company that offers its payment services to the merchants. While there are independent payment gateway and processing providers like Stripe or PayPal, credit card networks may cover these functions as well.

Accepting different payment methods (credit card, e-check, PayPal, GPay, Apple Pay, etc.) online would require working with different processors. Each has its own method for charging fees for transaction processing. For example, PayPal offers three pricing plans for processing transactions. The flat fee used by most merchants is quoted as 2.9 percent + $0.30 for every transaction. Other processors may differ.

The main purpose of working with a payment processor is to actually be able to transfer your funds securely between the banks. Additionally, payment processors and banks offer their gateway services, which eliminates the need to obtain special compliances to work with payments. So, what’s the difference between using a card network processor and a third party processor?

Payment processing by credit card networks and their fees

If you are a merchant, you basically have two options to consider. 1) You go to one of the third party gateway and processing providers that we described in a previous article 2) or go directly to credit card networks for gateway and processing services.

The cost of transaction processing is what differentiates the processors because it’s their main service. So now let’s compare the rates between the actual processor providers. In the following comparison, we’ll look at the pricing rates with each network, and look at a few third party payment processors to see the difference. We’ll also highlight some distinctions of working with each network provider.

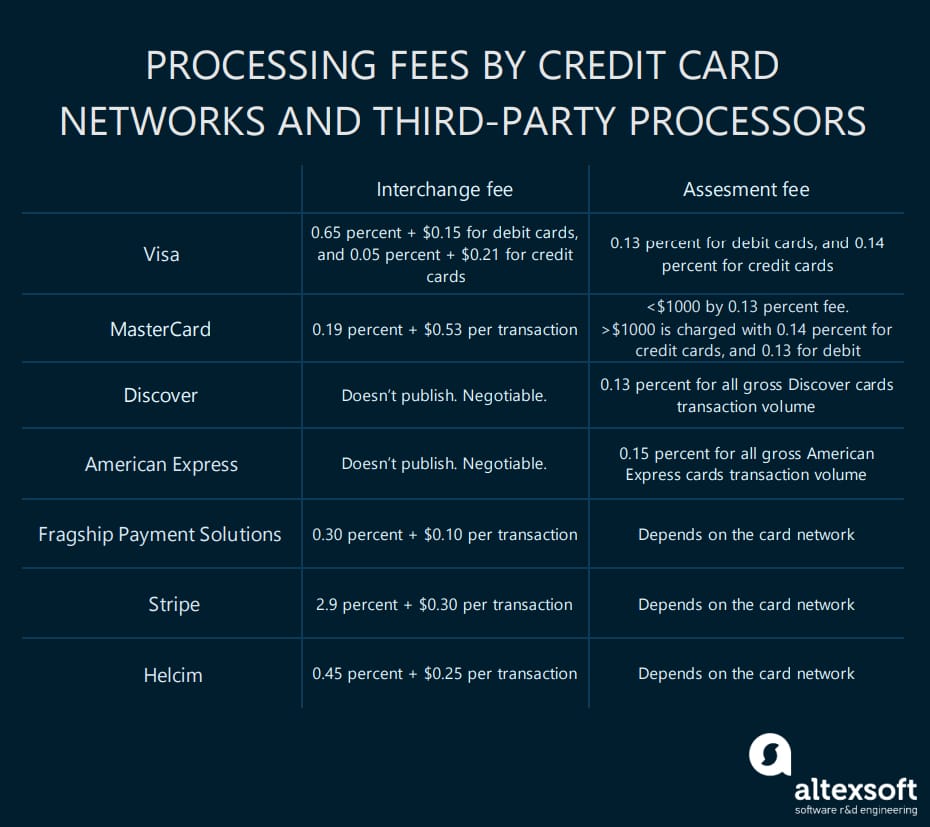

A quick look at the processing fees by networks and vendors

Visa payment processing

Visa is a US based credit card network. It operates as an open network, so banks can freely partner with Visa to become its issuing or acquiring bank. Here you can apply for a Visa merchant account and start working with the acquiring banks.

For acquiring banks, Visa offers an API that connects via the public internet to the VisaNet interface. The API performs a full range of transactions for online payments (authorize, settle, fund) with cards or tokens.

Interchange fees: Visa publicly posts its interchange fees annually. This can be found in the dedicated fee table describing all the possible payment scenarios. Let’s take an online card payment for retailers, which is 0.65 percent + $0.15 for debit cards, and 0.05 percent + $0.21 for credit per transaction.

Assessment fees: The main assessment commission by Visa is 0.13 percent of transaction amount for debit cards, and 0.14 percent for credit cards in the US. These assessment fees apply to all the debit/credit transactions via Visa cards. Acquirer authorization fees are $0.0195 and $0.0155 for debit and credit cards respectively. This fee is applied once per authorization.

MasterCard payment processing

MasterCard is also an open credit card network most popular in Europe. MasterCard promotes itself as a payment facilitator rather than payment processor. However, it operates much like Visa. To start accepting MasterCard credit or debit cards, you can contact any of its acquiring banks to get a merchant account.

Interchange fees: MasterCard also publicly posts its interchange fees. You can examine them by the link. MasterCard charges 0.19 percent + 0.53 for online card payment per transaction.

Assessment fees: For all the transactions less than or equal to $1000, MasterCard charges a 0.13 percent fee. Transactions larger than $1000 are charged 0.13 and 0.14 percent fees for debit and credit cards respectively.

Discover payment processing

Discover is another US-based credit card network. The main difference between the previous two and Discover is that it is a closed credit card network. Closed networks act as the acquiring bank themselves. So, on one hand, it allows for less flexibility. But on the other, transaction fees for the acquiring bank are exclusive in the closed network.

Here you can apply for a merchant account of Discover.

Interchange fees: Discover doesn’t post its interchange fees publicly but they are negotiable.

Assessment fees: 0.13 percent for all gross Discover cards transaction volume.

American Express payment processing

American Express also operates as a closed credit card network also known as Amex. And here is the link where you create a merchant account at Amex’s website. There you can easily apply for its online payment processing, which charges the following fees:

Interchange fees: American Express doesn’t post its interchange fees publicly but they are negotiable.

Assessment fees: 0.15 percent for all gross American Express cards transaction volume.

Third party processor

Now let's take a look at third party payment service providers and compare their interchange rates.

Flagship Payment Solutions offers processing for merchants, as well as creating a merchant account on their side. The interchange fee proposed by this processor is 0.30 percent + $0.10 per transaction.

Stripe is one of the biggest payment gateway/processor service providers. It also provides a merchant account for its users, and charges 2.9 percent + $0.30 per transaction.

Helcim is a full-service credit card processor charging 0.45 percent + $0.25 per transaction.

Keep in mind that a network assessment fee for each card brand will be applied to the transactions.

What is the benefit of credit card networks?

In choosing between processing your payments with a third party provider or a card network, you should clearly understand one thing. The card network is always present in the transaction processing because cards are validated by them. But choosing a network as your processor service brings several benefits.

Profitable rates. Depending on the card brand your customers use the most, you get more profitable conditions for transaction processing for the given card brand. It means, if you are a US based merchant, and your customers are also mostly from the US, they probably use Visa. So, you might save some money on their interchange rates.

Ecosystem of banks. The network is good as it is, because it allows you to use the whole ecosystem of partnered banks. For merchants, it means that with issuing banks, fees may or may not be lower. And with acquiring banks, you have a wide choice of trusted banks to create a merchant account at.

Security. To accept payments, there are standards you must meet like PCI DSS compliance. Credit card networks develop these standards. So, you eliminate the need to obtain them when using payment solutions vendors (valid for third-parties as well).

The downsides depend strictly on the actual network or payment processor fee rates. But, in most cases these would be

The need to cooperate with several networks. If you accept MasterCard, you can’t process Visa with the same network. As long as you want to accept as many payment methods as possible, this can be a blocker.

Inflexibility. With some networks, you’ll be bound to a specific bank as your acquiring bank. Which is not an option if you already have individual terms with your bank.

If you're just choosing a payment processor, sticking with a well-known option is a good idea. First and foremost, credit card networks are international organizations with hundreds of partnering banks. This ensures that your payments would be carried in a well-established, secure ecosystem. Which also guarantees a wide choice within a single ecosystem. So sticking with a credit card network as your all-in-one payment service provider can be a good idea.