How to Value a Fintech Startup

Compared to traditional financial services businesses, fintech startups require different valuation approaches. This article explores these differences and the best practices to apply when appraising a fintech investment.

Compared to traditional financial services businesses, fintech startups require different valuation approaches. This article explores these differences and the best practices to apply when appraising a fintech investment.

Nirvikar has helped raise $20+ billion of capital and built lines of business as an experienced CEO, banker, and strategist.

Expertise

PREVIOUSLY AT

Fintech is a popular contemporary buzzword and many of its products touch our lives every day. A fintech simply refers to a company that operates in the financial services sector and leverages the power of technology to simplify, automate, and improve the delivery of financial services to end customers. Further, they can be classified into various sub-sectors including payments, investment management, crowdfunding, lending and borrowing, insurance, cross border remittances, and so on based on the specific segment that they are trying to service.

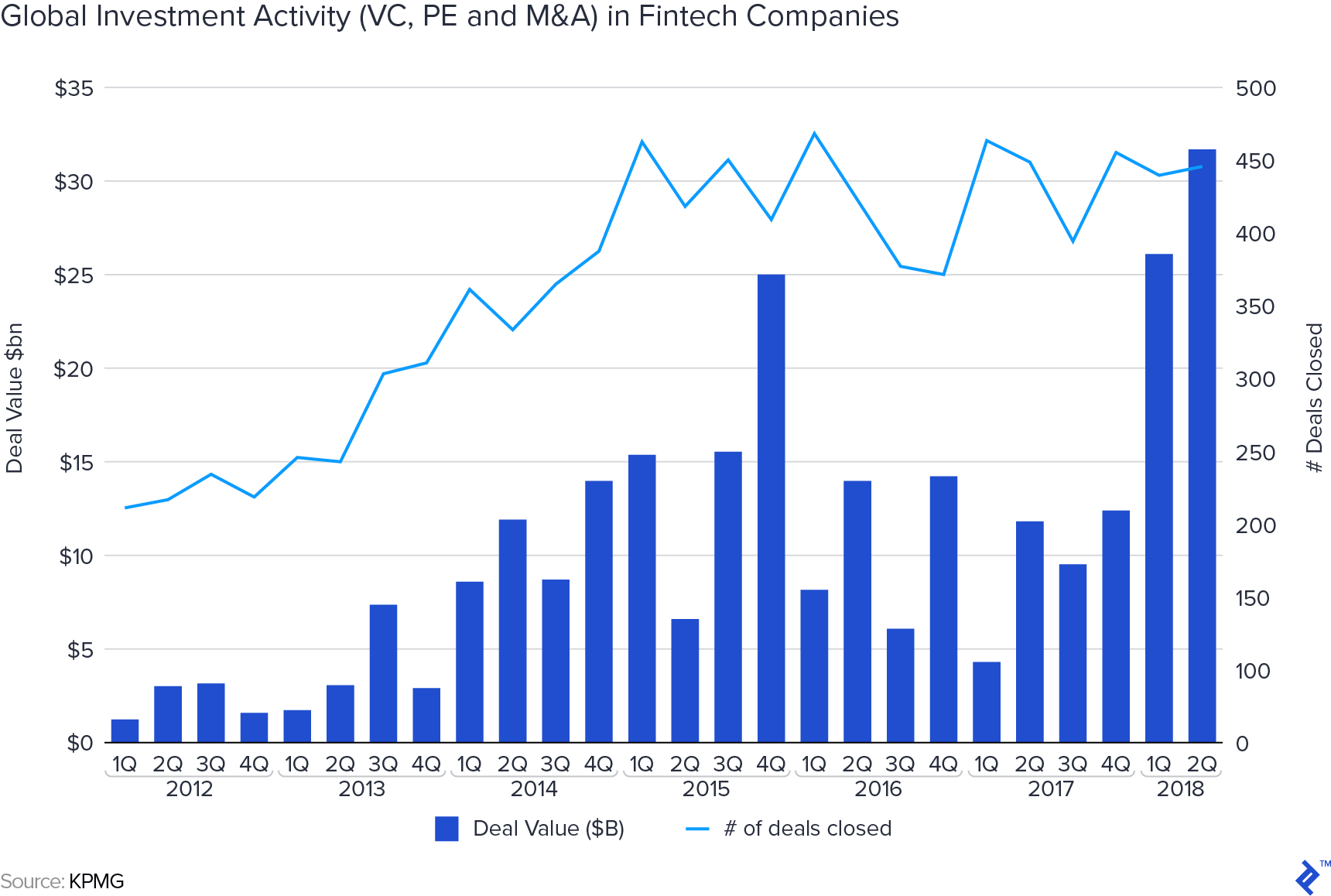

There were over 12,000 fintechs operating globally as of January 2019 (Crunchbase Dec 2018), who since 2013 have amassed total funding resources of well in excess of US$100 billion. In terms of the number of fintech startups, the US is the most active country, with India and the UK following. According to KPMG, global investment activity in fintechs exceeded $30 billion across 450 deals that took place in the first half of 2018 alone.

Company Valuation Approaches: Starting at the Top

The area that I would like to focus on with fintech is how its startups are valued. This interests me due to the following points:

- Why are some of these companies valued so highly, even higher than existing brick and mortar banks, asset management companies, or insurance companies which have been in existence for decades?

- What makes these startups reach such high valuations in such a short span of time? Are these valuations real or imaginary?

- Is there an underlying logic or are these just based on sentiment and market hype?

These are some of the issues that I am going to try and address in this article.

First, let me highlight some of the traditional valuation models that are conventionally used while valuing companies. These methods include:

- Discounted cash flow (DCF): Traditional model that discounts future cash at the average cost of capital to arrive at the present value of enterprise/equity.

- Multiple of revenue or book value: Such models use a multiple of either revenue or book value to arrive at the value of the company

- Replacement cost: If the business being acquired has assets that are hard to replace or will take time and money to build, one can use the replacement value of underlying assets as a benchmark for valuing the company

- Price-to-earnings (PE) ratio comparable: PE multiples of future earnings per share (EPS) is another common method of valuing companies.

- Strategic/competitive value: A company may bid for another competitor that could potentially become a threat to its existence (i.e. Facebook’s takeover of WhatsApp) and put its business model in danger.

Most valuation exercises use the multiple method to arrive at the valuation of a company and then use different approaches to arrive at ranged estimates, before choosing a number that matches their overall strategic, business, competitive, and return requirements. One thing to note is that the above approaches are typically useful for mature, stable businesses with relatively predictable cash flows and established business models. Whichever approach is used, they are all the same in just trying to estimate an outflow and future expected cash flows with an expected range of IRR.

However, when one looks at the current crop of fintech startups, all of these principles look difficult to apply due to them having completely unpredictable or even negative cash flows, rapidly changing pivoting business models, and in most cases, negligible physical assets.

Valuation of Financial Sector Companies: Traditional Approaches

Now let’s be more specific and look at the valuation of financial sector companies. We can broadly divide the finance industry into various sub-sectors as described below. Each has certain nuances that affect how valuation can be applied to their specific business models.

Banks

Modern global banks are typically aggregations of commercial banking, investment banking, wealth management, and advisory services. Focusing on the “traditional bank”, a conventional commercial bank would be valued on parameters like net interest margins, return on assets, EPS, and comparable PE multiples. The first two parameters measure the efficiency of the bank and how efficiently capital is being deployed, while the other two are measuring returns that accrue to shareholders, taking into account the capital structure and the expected growth in earnings.

These approaches primarily take into account the business model of a bank, which basically runs on the spread between deposit and loan rates while managing defaults and maintaining an efficient capital structure.

Mutual Funds

Asset management companies (AMCs) are typically valued as a percentage of AUM that measures an AMC’s ability to generate cash flow based on the total size of funds that it has under its management. This can vary based on the underlying asset class breakup of equity vs fixed income, fee structures and so on.

Another popular measure is to look at market capitalization to AUM, which aims to correlate growth in income potential with the size of the fund, based upon an underlying assumption that AMCs with very high AUMs will not be able to grow income as fast as smaller ones. Other variables to keep in mind while valuing AMCs are:

- Size of the absolute investor base.

- Growing vs stable base of investors.

- Public and regulated vs private and less regulated fee structures.

Insurance Companies

An insurance company would typically be measured on common parameters such as return on equity. A good surrogate for value companies in the public markets would be price to book value, which will reflect the relative valuation of companies across markets. More specifically, some of the relevant factors for valuing insurance companies would be as follow.

Premium growth in the market/company. How fast is the company’s premium income growing? Is it gaining market share? Is the underlying market saturated, or growing? Naturally in a market where insurance is still gaining popularity, the former will likely have a higher potential for growth. Similarly, a new company is likely to have a higher potential to grow as compared to an existing market leader.

Returns consistency. In the case of insurance companies, the payout ratio is not a clearly predictable ratio and can be volatile. Hence one measure that we look at when valuing an insurance company is the consistency of its income to ascertain whether over longer periods it makes consistent returns.

Other comprehensive income (investment income). An insurance company’s income comprises of premium income and investment income earned from its investments, hence OCI is a measure that shows the level of returns from its investment portfolio and forms one of the two key sources of income.

Wealth Management Firms

Conceptually it would appear that WM firms are akin to AMCs and their valuation would be correlated with AUMs, revenue and fee rates. However, their business models are different to pure mutual funds, whos setups are more institutional and standardized. Fund managers do add value, but their investments are more process oriented to support large AUMs driven by standardized and regulated products, with a mass-market sales approach.

In comparison, wealth management firms are more boutique-y and are comparatively less regulated, thus the value that investment managers add is customized to the risk appetite of clients. Also, in the case of sales, relationships are key, with loyal clients investing based on their personal trust, comfort, and relationship with a manager.

Hence, valuing a WM firm is a more detailed and complex task that needs to go into a number of variables. So when valuing a WM, one would have to add the impact of these variables in the valuation model before arriving at a final number.

Understanding the Components of Fintech Valuation

When we come to valuing fintechs, the key differences between conventional businesses and early businesses are mainly in terms of:

- The nature of the problem that it solves (something that wasn’t possible earlier purely due to a breakthrough in technology).

- The ability to rapidly scale up across vast geographies without having the need to set up physical presence and infrastructure.

- The lower cost due to lean structures that no longer needs vast physical IT infrastructure and manpower required by conventional banks.

All these variables give insights into the kind of TAM available, and the subsequent revenues that the fintech can generate.

Below are some of the key variables that go into qualitatively assessing the potential of a new generation fintech, as compared to the traditional financial sector companies that I described above. Let’s take a detailed look at some of these variables

1. Problems Solved

The foremost variable is the nature of the problem that is getting solved by the company, whether it’s a disruptive solution to a major problem or just an incremental improvement in an existing solution that may not affect the incumbents in a big way.

Using Fintech as an example, Transferwise has grown to a valuation of $1.6bn, due in part to it changing the paradigms of money transfer. If it had followed the status quo of analog brokering based on FX and payment cost, then it’s most likely that it would not be as successful as it is now.

2. TAM/SAM

The nature of some businesses makes them easily scalable across large geographies. For example, in the past, banks or mutual fund companies would need an extensive infrastructure of offices, branches, distributors, and agents to be able to reach and service their customers. With new age mobile-enabled fintechs, they are accessible to a client across the legal geography that they operate in and hence can rapidly scale up business.

This allows them to cover a very large TAM within a relatively short time frame hence. For example, digital bank fintech Revolut was launched in 2015 and already has over 3 million customers and is available in over 120 countries. This is definitely larger than the number of countries served by most large international banks which have been in existence for over 100 years.

3. New Use Cases

As fintechs innovate there are new use cases that are enabled with the help of technology, which can potentially expand their market. A simple example could be a drastic reduction in cash balances that customers keep, as fintechs enable low-value P2P payments. This, in turn, is likely to increase idle balances kept with the fintech, as compared to traditional bank accounts. A real example in the fintech world is from wallet startups like Paytm using P2P transactions for enabling low-value payments to settle transactions amongst friends, splitting bills and making payments to small businesses.

4. Lower Distribution and Setup Costs

Typically such startups have business models that leverage the power of networks and are themselves very lean, with much lower infrastructure and setup costs. These costs can reduce as the size of the business grows and customers may benefit from this. For example, Uber doesn’t own any cabs or doesn’t need to have a huge setup for owning, servicing or maintaining cars. In the fintech world, companies like Revolut, Transferwise, and Paypal have a wide footprint across the world without having the need to open offices in each location.

5. Lower Operational Costs

In line with lower infrastructure and manpower, these companies have much lower marginal costs, as the business models are tech-enabled, rather than with transaction-linked high variable cost. This also makes these business models profitability increase exponentially after a certain critical mass that absorbs the fixed cost structure. In the fintech space, one can look at companies like Monzo which have less than one tenth the cost of servicing a retail account as compared to a large traditional bank.

6. Revenue Models

Fintechs work on revenue models that leverage the power of a large number of customers and transactions that network effects enable. It’s important to understand what is the revenue model and how are they going to eventually make money, be it directly from the user or indirectly via advertising or data plays. A model that is just based on generating users without a clear understanding of how it will be monetized may not be successful in the long run.

7. Cross Selling

Due to the typical platform nature of a Fintech offering, it’s also easy to continuously keep adding features and products to the initial MVP.

Cross-selling opportunities become apparent with the benefit of AI-supported insights about consumer behavior and patterns from their use of the tech. This makes it amenable to continuously expand the scope of the offering with relatively small effort. An example of this can be the UK retail bank Monzo which originally started as an online prepaid card service, then a current account and now, lending services.

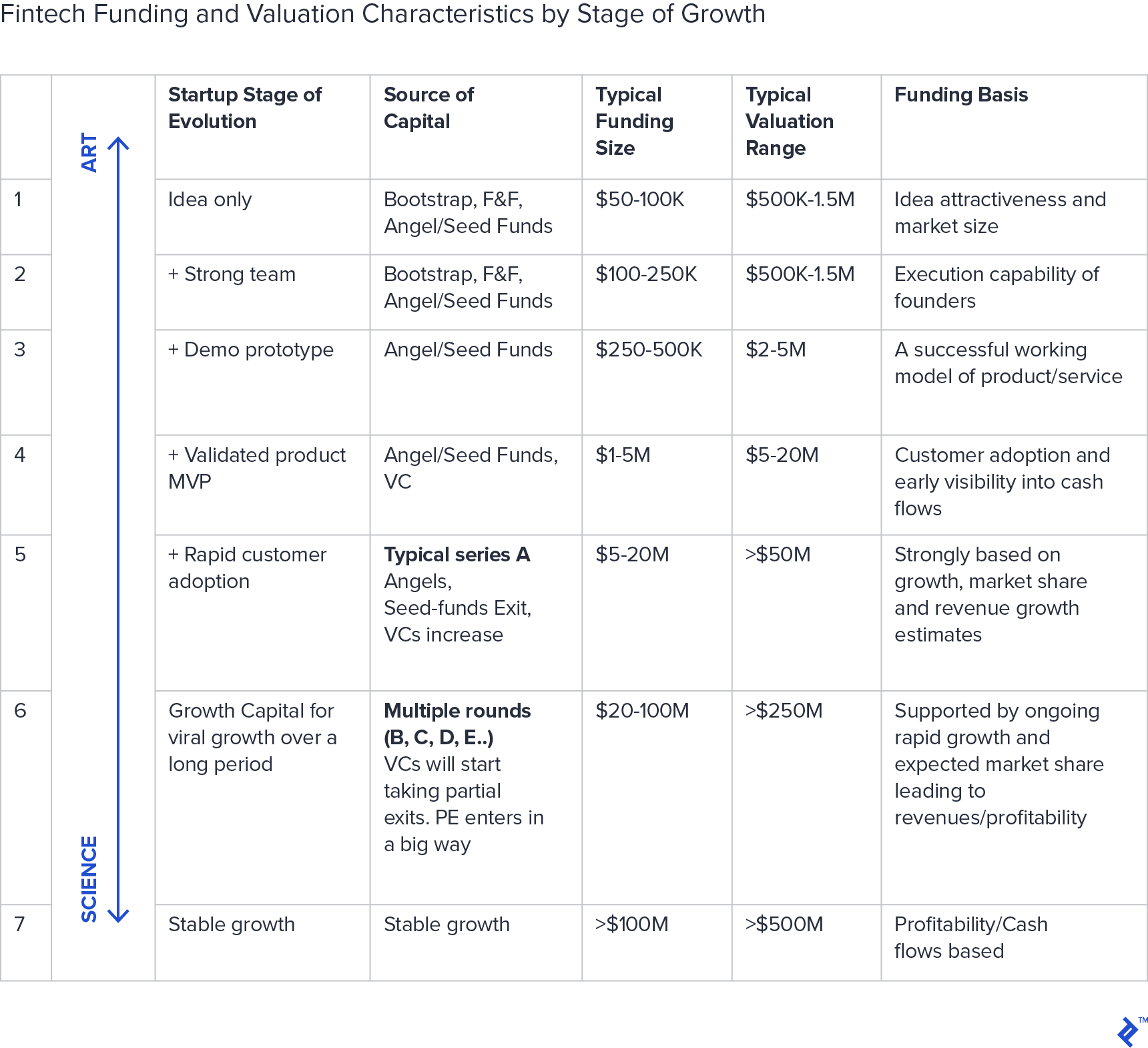

The Stages of Fintech Development and Investor Profiles

Let’s look at the life cycle of a fintech company and understand each phase.

Starting Out

Once an appropriate founding team is formed, the next step is to convert the idea into a prototype product or service. This prototype is typically a very basic version that translates the vision that the founders have into reality and tries to demonstrate and visualize how the new product will solve the problem in a different way. At this stage the idea is typically funded either by bootstrapping, friends and family, or angel/seed investors and could involve a total initial investment of between $50,000-100,000.

Post founding, the startup uses money raised to build a simple MVP that is a functional and robust working model that can be tested in the market for acceptability. This is an important step in the evolution of the startup and it may require multiple iterations with its functionalities/features to get the product right, using customer feedback loops.

Gaining Traction

Once success is achieved in this, the startup is now ready to raise the next round of money, once again from the angels, seed funds, or VCs. At this stage, the startup has a valid idea and a successful MVP that now needs to be launched in the market to build customer traction. The startup will likely raise the next round of growth capital which could range from $250,000-2 million and can come in multiple tranches based on meeting agreed on milestones.

Full Steam Ahead

Once the company achieves rapid product adaptation and its evident that the customer acceptance is strong and the product will likely scale up, it’s time to now scale up the business, build a robust organizational structure, hire bigger teams and build formal structures. This is the stage at which the company will raise Series A funding, where most early angels/seed funds will likely exit and VCs will increase exposure. Conceptually, the startup has now graduated to a lower risk state and hence there is a switch in the class of investors based on risk-reward expectations.

From here on it’s a stage of rapid growth which will lead to multiple rounds of VC/PE funding and fuel a rapid growth of functionalities, geographies, team sizes and even potential acquisition of competitors or synergistic companies in the entire ecosystem. This will go on until the company’s rapid growth path stabilizes to a more predictable growth path, which will ultimately result in the company launching a public offering (IPO) and an exit for all the remaining investors.

All of this can broadly be summed by the following infographic:

How to Value a Fintech Startup: Valuation Methods

Unlike the traditional financial services business valuation methods described earlier, Fintech, like most startups, has specific approaches that are used for appraising investments.

Scorecard Valuation Model

In scorecard valuations, you first start with estimating an average valuation for similar companies and then asses the target company to this based on a range of parameters. These weightings are applied judgmentally based on the investors’ assessment of relative importance (all of them add up to 100%), with the total rating quotient being applied to the average industry valuation for an indicative mark.

Berkus Method

A quick and easy method to value a startup, based on the expected revenue reaching at least $20 million. That being the case, the startup is evaluated based on five parameters: soundness of idea, founding team, having a product prototype, existing customers and existing sales volume (however small maybe). Based on the attractiveness of each of the above variables, a maximum valuation of $0.5m is applied to each, ensuring that the total pre-money valuation has a maximum cap of $ 2 million.

Risk Factor Summation Method

This method approaches valuation from a much broader perspective and considers a selection of 12 parameters.

Each of the parameters then rated on a 5 point scale (from +2 to -2), multiplied by a factor of $250,000 and then summed up to give the total indicative valuation.

Cost to Duplicate Method

Like in the case of a mature business, if a startup being acquired has the technology or team setup that will take time and money to build, one can use replacement value, or cost-to-duplicate as a benchmark for valuing the company. While this is conceptually similar to the replacement cost method in case of mature companies, the difference here is that the focus is on the broad setup and technology team, rather than physical assets or production capacities.

Venture Capital Method

In this case, the investor typically works backward, by looking at the returns that he is expecting on his investment, based on the exit value estimation of an attractive startup. Let’s say if his return expectations are 15x and he expects the exit valuation of the startup to be $15m, then the present post-money valuation of the startup is calculated by:

Exit valuation/Return Multiple = $15M/15x = $1M

This would be the current post-money valuation of the company, so if $250,000 is being invested for 25% of the company, then the pre-money valuation of the company would come to $750,000.

Others

In addition, there are a few other methods which have been explained above but are primarily used in case of mature companies, I have listed them below for your convenience.

- DCF (Discounted Cash Flow Method)

- Multiple of revenue or profit

- EBITDA Multiples

- The Book Value Method

Art or Science? Depends on the Stage

We can see that at the early stage of the valuation of a fintech is more an ‘art form’ based on vision, market size, promise, dreams, and subjective judgment. As it progresses through its life, it then increasingly becomes more scientific and data based on market share, revenue and cash flows.

Ultimately, it is the potential cash flow that determines the value of a startup, all the above methods can be taken as routes towards calculating this simple concept and the resultant ROI that the investment will generate. These methods are all various surrogates that basically try to calculate the cash generation capability of the business in the long term.

I will continue to explore these concepts in a future article, by applying the above principles to value Transferwise, the UK based cross border money transfer company that has disrupted the cross border money transfer space.

Further Reading on the Toptal Blog:

Understanding the basics

What is a fintech company?

Fintech companies are financial services businesses that specifically focus on developing technological innovations to increase their reach, product capacity, and cost attraction to a customer, within the provision of financial services.

Nirvikar Jain

Stanford, CA, United States

Member since June 14, 2018

About the author

Nirvikar has helped raise $20+ billion of capital and built lines of business as an experienced CEO, banker, and strategist.

Expertise

PREVIOUSLY AT