Late last week, Turo, a startup that allows consumers to rent their cars to one another, updated its IPO filing to include full-year data from 2022, giving us a better understanding of its post-COVID performance.

Turo, a venture-backed company that has raised hundreds of millions while private, filed privately to go public back in 2021. That initial document was converted into a public filing the next year, with Turo updating its S-1 documentation regularly since — most recently to include Q4 2022 data.

The Exchange explores startups, markets and money.

Read it every morning on TechCrunch+ or get The Exchange newsletter every Saturday.

While TechCrunch and other publications have discussed unicorns like Instacart and Reddit as potential companies first out the IPO gate when the public-offering window reopens, perhaps we were looking in the wrong places. Turo could be the first.

A Turo IPO would not be a small affair. PitchBook pegs the company’s most recent private-market price at $1.28 billion, making it a unicorn long in the making, having raised capital as early as 2009. Readers may recall that Turo was once called RelayRides and has over time extended its model to support users offering more than one car for its platform.

Let’s sit down and look at Turo’s numbers in detail and dig up what we can from the recent rocky SPAC combination of Getaround, which has a similar model and may provide valuation clues for Turo. To work!

Pretty good, really

Turo’s recent financial data is pretty impressive overall, though we need to chat through some of its metrics in detail. Here are the broad strokes:

- In 2022, Turo’s revenues grew 59% to $746.6 million from $469 million in 2021. The company’s performance in the last two years represents a dramatic change from its $141.7 million and $149.9 million in top line for 2019 and 2020.

- That rapid growth changed Turo’s profitability aspect. After reporting an operating loss of more than $100 million in 2019, its operations lost another $55.7 million in 2020.

- After its massive 2021 growth spurt, Turo became profitable on an operating and adjusted EBITDA basis. In 2022, it also posted strong GAAP net income. Given how its income statement reads, we care a bit more about its operating income than its net income results; the former is a better indicator of its unadjusted health.

A company growing 59% year over year during uncertain economic times, posting record net income while recording nearly three-quarters of a billion dollars in revenue against a roughly $1.25 billion valuation? What’s not to like?

There are some modest quirks to discuss. These include Turo’s operating profitability slipping in 2022 to $33.8 million and its operating cash flow falling from $108.0 million in 2021 to $41.0 million last year. Sales and marketing costs also roughly doubled last year.

Still, it’s a healthy company with more than $300 million in cash and a lot to be proud about. Is there any real reason for concern? Or, put another way, why isn’t it going public already?

Getaround’s SPAC mess

Let me catch you up on the last few years of Getaround news. The company, which operates a pretty similar business to Turo, raised $140 million “amid a rebound in short-distance travel” back in 2020. Fast forward to 2022, and this column noted that Getaround’s expected SPAC combination made some sense as it needed the cash and was likely optimizing for cash accretion.

In December of last year, we reported that after its SPAC merger, Getaround’s share price had cratered by around 70%. Its valuation losses have continued.

Last month, Getaround was in danger of being delisted by the NYSE for falling under a $1 per share price minimum, and the company laid off staff. Today, it’s worth around 28 cents per share, giving it a market cap of around $25 million, per Yahoo Finance, or loosely the value of a large Series A.

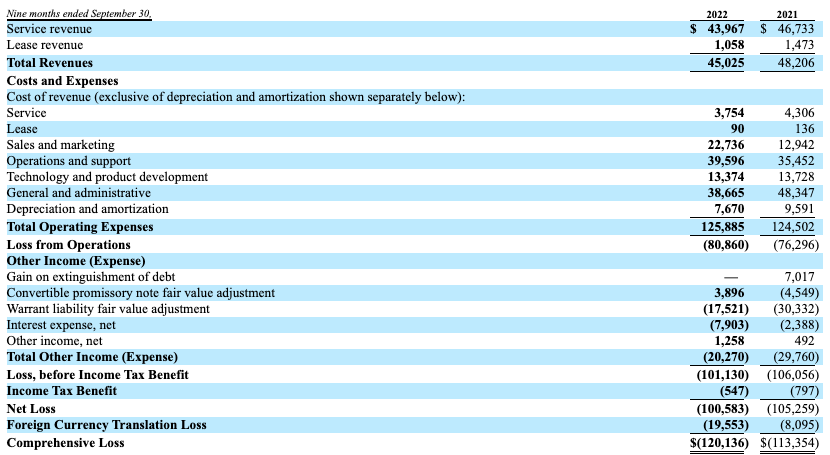

The last data from Getaround comes from early December, right before it closed its SPAC combination. Covering results through Q3 2022 (we lack more recent data, oddly), here’s what we were looking at back then:

Image Credits: Getaround SEC filing

After skimming that, you should punch me in the shoulder; why would I compare a profitable company with lots of growth to one that is shrinking and losing money?

Listen, don’t get mad at me; I am not trying to say that Turo should be wary of a public offering at the moment due to Getaround’s woes. I am, instead, trying to say that Turo might be waiting for the Getaround mess to clear itself from the public markets so that when it does price its IPO, it isn’t stuck with a single comp in the market that isn’t doing well.

Because the two companies have wildly diverging results, we cannot use the Getaround valuation to help price Turo. Instead, we can run a little thought exercise:

- Turo is an asset-light, software-driven company that has gross margins of above 50% in the last two years.

- It has posted strong growth in recent years and is more than capable of self-funding while generating comfortable profits.

- Thus, it is worth at least 2x its trailing revenues.

Why do we care whether or not Turo is worth 2x its trailing top line? Because at that lowball figure, it’s worth more than its final private price. Put another way, Turo is not in danger of a down-round IPO, at least not looking at the numbers we have in front of us. Thus, it is merely waiting for a prime market moment. Between banking stress and Getaround pancaking after leaping into the public markets, well, this probably isn’t it.

Still, we must nearly be there, right? Turo probably wants to price its IPO while its 2022 results are still in people’s minds, as they are rather good.

Please, Turo?