Vishal Lugani

I have recently been a part of a few M&A processes at companies I work closely with. These transactions involved private companies selling to larger companies (public and private) and were all-cash transactions.

This inspired me to chronicle best practices and considerations for founders who are selling their company. In doing so, I hope that founders take away at least one useful insight.

I am grateful and fortunate that I could solicit input on this article from several people, including Theresia Gouw and Mark Kraynak; a few of my partners at Acrew; Ed Zimmerman and Meredith Beuchaw from the law firm Lowenstein; Shan Aggarwal, VP of corporate development, Coinbase; and Art Levy, chief strategy officer at Brex. I hope to also hear from more founders as they read through this.

First, some observations

M&A can be a great outcome for all parties, especially for startup founders and their team. Founders may have conflicting emotions when thinking about selling their company. That is perfectly understandable; in the beginning, many founders hope to build an enduring company.

However, it’s important to acknowledge that there are plenty of good reasons to sell: You can join a “larger rocketship” where 1+1=3; there could be a strong match with an acquirer; burn-out in the startup team; the team or investor wants liquidity; and so on. Further, myriad long-term, standalone companies have been founded by founders who sold or exited their prior companies.

During downturns, think of M&A as a game of musical chairs. The companies that test the market earlier in the cycle (before things have gotten particularly bleak) tend to see better outcomes.

In markets where incumbents are playing catch-up, there is a window when a few companies will get bought. By the time those deals settle, the rest will likely decide to build instead of buying.

Below, I’ve outlined the key steps of a M&A process.

From a timing point of view, founders should plan to conclude a sale in up to nine months. That isn’t to say it can’t happen sooner, but we would counsel that amount of cash buffer. This may require companies to raise bridge financing and/or consider reducing burn. As one of my partners counseled, “Every week you wait to cut spend makes the cuts you will need hurt that much more.”

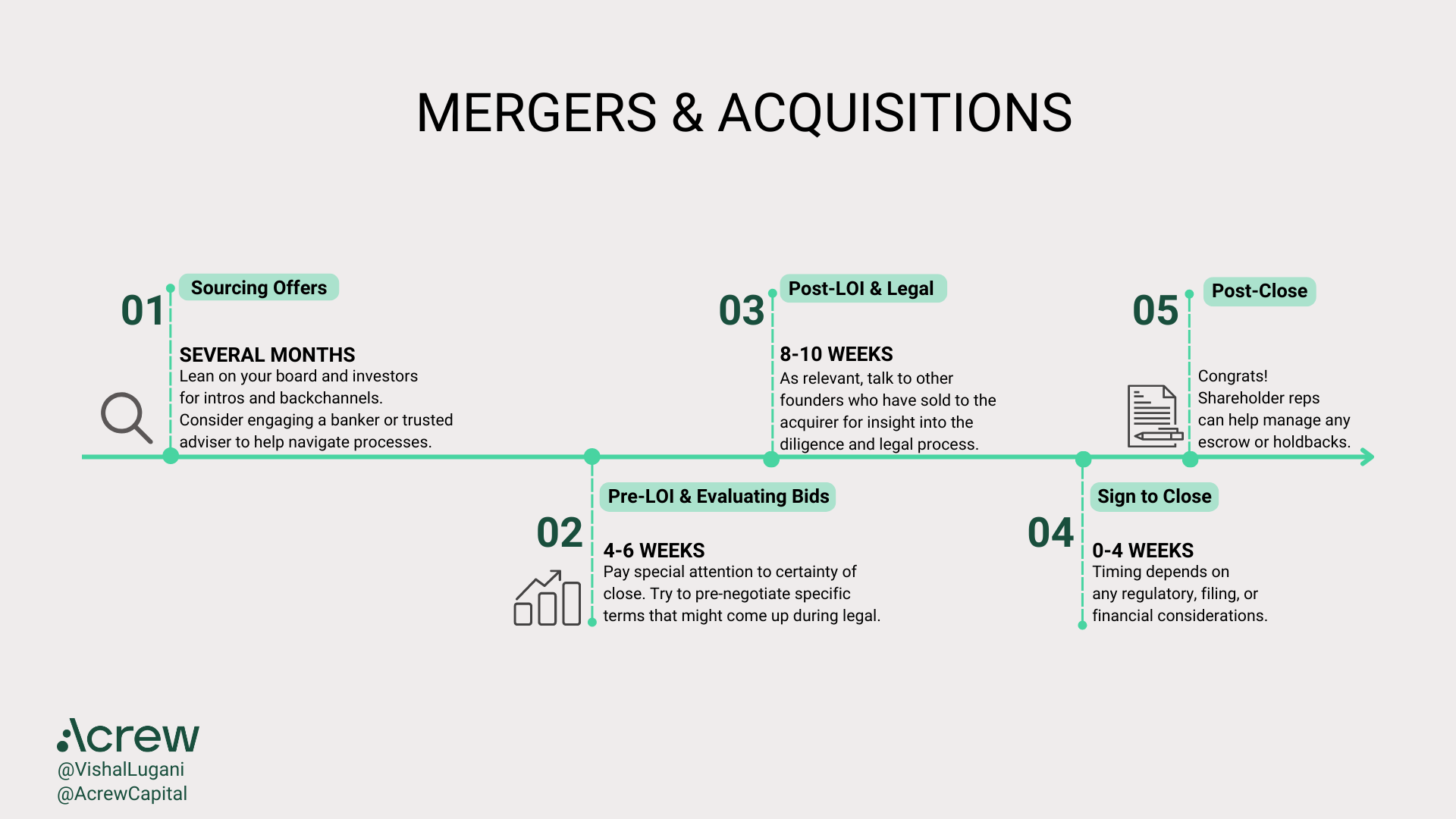

Sourcing offers

- This entails months of building relationships. Before a process, finding offers could take anywhere from several weeks to a few months to get all parties engaged and working.

- You’ll want to share any offers with your board and key investors to make sure you’re atop all governance requirements.

- It’ll be useful to build relationships with bankers as well, because they are in the market and talking to acquirers frequently. This will help you stay top of mind in your industry and be included for everything from conference invites to market maps.

Pre-LOI and evaluating bids

- Again, this can take several months. A highly motivated acquirer running a tight process should be able to get through diligence in two to four weeks, but that would be fast in any market. You need to account for competing priorities at the acquirer, any other deals that might come up for their corporate development and personnel schedules.

- Your leverage declines after you sign a LOI. In many cases, the LOI puts you into a period of exclusivity with the buyer. That’s why it’s important to nail down the details on the terms right away.

- Consider getting representation and warranty insurance (RWI). This will influence how much of the deal consideration is paid upfront and how much is “at risk,” where selling shareholders will be at risk of losing proceeds earmarked or distributed to them.

Post-LOI confirmatory and legal diligence

- Generally, diligence at this point should be less strategic and more operational. Legal diligence, however, will be exhaustive, and you may find that more detailed terms are being either negotiated or renegotiated via definitive long-form deal documents. It’s important to plan for this process with your legal counsel.

- If you opted for an RWI, the insurer will also run diligence on the company.

Sign to close

- You will then get to the final purchase agreement — often in the form of a merger agreement — and collect all the required signatures, including the shareholder approvals.

- The deal will not close for at least a few weeks after you’re done signing. The timing of the close will depend on whether there are any regulatory, filing or financial considerations. We advise founders to focus on when the cash is in the bank, so to speak.

Post-close integration

- Consider having a shareholder representative manage post-deal claims and payouts of whatever cash is held in escrow or as a holdback with RWI.

- This is your time to ramp up and focus on execution. If this was a good match between companies, a lot of value can be created at this point.

With that context, here are a few factors to consider during M&A:

Get to know your acquirers before the process

It’s always preferable to have existing relationships with acquirers. This is easier said than done, however.

First, I don’t know too many founders who, a priori, think about their startups being bought by a specific set of acquirers, but it’s worth the time. Potential acquirers are often either good partners or competitors.

One of the many plates a CEO should be spinning is keeping the heat on accretive partnerships. This should be helpful irrespective of whether a founder decides to sell. Further, some engagement with competitors (e.g., at trade shows and conferences) can also be helpful.

Ensure you have multiple conversations with acquirers

The best M&A outcomes typically involve a few potential acquirers who get to the later stages (i.e., discussions about price).

In such cases, timing conversations so they move along at a similar pace is important — if one party moves faster, you can use that as a way to speed up other parties.

Even when you receive an inbound offer from a highly motivated potential acquirer, engaging other parties should be best practice. When you’re single-threaded, you introduce considerable risk to the process. A potential acquirer only needs to miss your deadline once to realize they are the only one in the process.

Financial advisers can help at this stage, as bankers can help drum up additional acquirers. It’s easier to engage a banker sooner than later in the process.

Personal advisers who have been through M&A as operators before could also be helpful. This could be one of your investors or board members, someone well versed in corporate development or another founder who has been through M&A.

If you receive any pushback on running a process from any of your potential acquirers, you can always remind them that you have a board and investor stakeholders to manage and, furthermore, you have a fiduciary responsibility to the company (assuming you are on the board) to get market feedback on pricing and terms.

Selecting an acquirer

At some point, you’re going to have to decide on an acquirer. You, your team and your board/investor group will want to consider a variety of factors. Occasionally, founders will have the luxury of choosing from acquirers and can take into consideration which company will give their product and team the best shot at continued growth and success.

It’s relatively rare, though, for founders to be able to operate as they used to. Acquirers have a broader set of plans at play. In most instances, founders will have to understand that they are selling and will become an employee. They must introspect if they can spend one or more years at the acquirer, and consider what they might receive in return (such as financial reward, good landing/outcome for the key stakeholders, or continued employment and reward for team members).

In addition, in this volatile macro environment, it’s paramount to consider the probability of a deal actually closing. These M&A processes can be long, and the last thing you want is a transaction near the end of the road only for the company to be low on cash and the deal to fall through or get re-traded. It is not uncommon to accept a lower price if the probability of closing is higher, within reason.

To this end, it’s critical to understand why an acquirer wants to buy your company. Is your company getting bought for its product, business or team? Do you understand your relative position in the negotiation? For example, are there other options on the market that the acquirer could pursue, including simply building what they want themselves?

Other factors to consider include:

The process to close (approval process)

What does the decision-making process and timeline look like?

The relative weights of the different stakeholders you are dealing with

- Who is your sponsor in the product or business organization?

- How much visibility does this acquisition have at the acquirer’s executive and board level?

- How empowered is corporate development? Have they (the specific team) been involved in many deals before?

- Are you confident that the parties you are dealing with (corporate development, product/business champion, key executives, etc.) are feeling settled in their roles? This piece can be hard to suss out, so you’ll have to use your intuition. You likely don’t want your key champions to leave halfway through the process.

Any other positive or negative incentives at play

If you are selling to a public company whose stock has been hammered (as many have lately), consider how the broader environment may influence their willingness to, say, negotiate on price. Also consider how willing they might be to pay cash or stock.

The integration plan

This part often tends to be overlooked in the M&A process, where the focus is on deal terms. Founders and their teams will want to pay attention to how they fit into the company they are joining.

Put corporate development on speed dial

Once you’ve evaluated the certainty of closing, you’ll want to understand corporate development’s MO.

We’ve been in transactions that were the first corporate development-led acquisition for big acquirers. This can create friction, because when a company hasn’t built the organizational muscle of acquiring other companies, it’s likely the playbook is being built on the fly and even likelier that the integration will also be somewhat ad hoc.

Further, with new corporate development teams, it can be hard to understand how they will behave because there won’t be a list of founders with whom you can consult.

In either case, corporate development will likely be an important part of the triangle of influence at the acquirer, which will also include your internal stakeholder/product leader and the executive team/board.

Dealing with legal eagles

Understand the dynamic between internal general counsel (should there be one) and external counsel. If the acquirer has a formidable legal team, it’s advisable to reference that team if you can.

We’ve had instances where we’ve been on the other side of law firms that ask for legal terms that we understand are off-market — e.g., certain indemnity clauses, onerous founder revesting, etc.

You should hope that the external counsel is well versed in helping the acquirer buy venture-backed companies, as opposed to, say, private equity-backed companies or even bootstrapped companies. Why? Venture capital involves the purchase of minority stakes, and startups often have a diversified cap table. There will always be differences among investors, and different firms will have invested in your company at different times.

In either case, opposing counsel can make life quite difficult. That’s also why it’s important to have legal counsel on your side who is well versed in M&A and has been part of a recent slate of processes.

Often, you will negotiate what the “market” is. Ultimately, the terms are somewhat of a function of how much leverage each side has, but it will make your job easier if you work with a law firm that can credibly claim to be “in market” consistently.

Finally, even legal issues can be resolved between business stakeholders. All this involves give and take, and it’s ultimately your job to manage all the parties, including in the legal process. Collect information, get good counsel, ask other founders and investors, and use your judgment.

Keep your team motivated and maintain momentum

For startups, the best processes are often run with a small set (i.e., not all) of founders and the executive team. Our general advice is to minimize the team’s exposure to the M&A process to reduce distraction.

That said, employees may well want transparency, particularly around runway. Use your best judgment and balance your optimism (or pessimism) with keeping the team focused on the business at hand, and consider using specific tactics where needed to retain key talent (e.g., stock awards tied to an M&A outcome).

On the last point, once you have a term sheet (as in you’re raising venture capital too), your 409A will be invalid. One solution to this is to negotiate new incentives for employees at deal closing as part of the term sheet. If that doesn’t work with the acquirer, you could discuss carving out cash bonuses for employees, though this will reduce the deal price.

Managing your investors

Just like with your employees, you will want to communicate with at least a subset of your investors, as consistent with the confidentiality agreement your company has signed with an acquirer.

Your board should be kept in the loop throughout the process. Your board of directors can help field new acquirers, and it’s important to remember they also have obligations, as per corporate law, to conduct a proper process. Board members can also help create competitive and timing pressure. They can be the group you blame for not conceding on terms an acquirer is asking for. And, they can help get other investors on your side.

It’s important to check with your counsel what the communication cadence needs to be with your shareholders, investors, as well as major third parties whose consent might be required — as a condition to or simply as a result of the deal. Generally, a sequence of events will trigger communication with your board, and then another will trigger communication with your larger investor group.

You also want to understand what the approval thresholds look like — i.e., who you need, from which class of stock and/or other securities, to approve a transaction. Note that buyers will often ask for an approval threshold higher than what is required by your company’s governing documents.

Driving to close

Like any fundraising or sales process, you have to keep the pressure on. There are a variety of ways you can do so, but the key thing to highlight here is that once you’ve decided to sell the company and finalized a price, it’s in your interest to close as soon as possible.

Time kills deals, and time during downturns only introduces more risk. To the extent an acquirer comes up with new diligence findings or there is a change in the market, it is possible that they will re-trade the headline price and other key terms.

Also, you’re likely consuming cash as the process drags on. Proceeds are going to be net of your cash, so the sooner your close, the better for all.

In conclusion

Not all companies are best positioned to go it alone, and that’s okay. Further, many founders will exit only to build very successful second, third or fourth companies. Good luck as you navigate this environment and thanks for reading.

Comment