Another day, another 52-week low.

It seems that instead of finding fresh support, the value of software companies keeps discovering new basement levels to descend into. This afternoon, software stocks were off 3% or so, while the broader Nasdaq composite was down around 2% in mid-afternoon trading.

The dramatic collapse in the value of software stocks has been a key story starting when the trend began in late 2021. Since then, the value of a dollar of software revenue has been cut, slashed, beaten back, and then kicked in the shins.

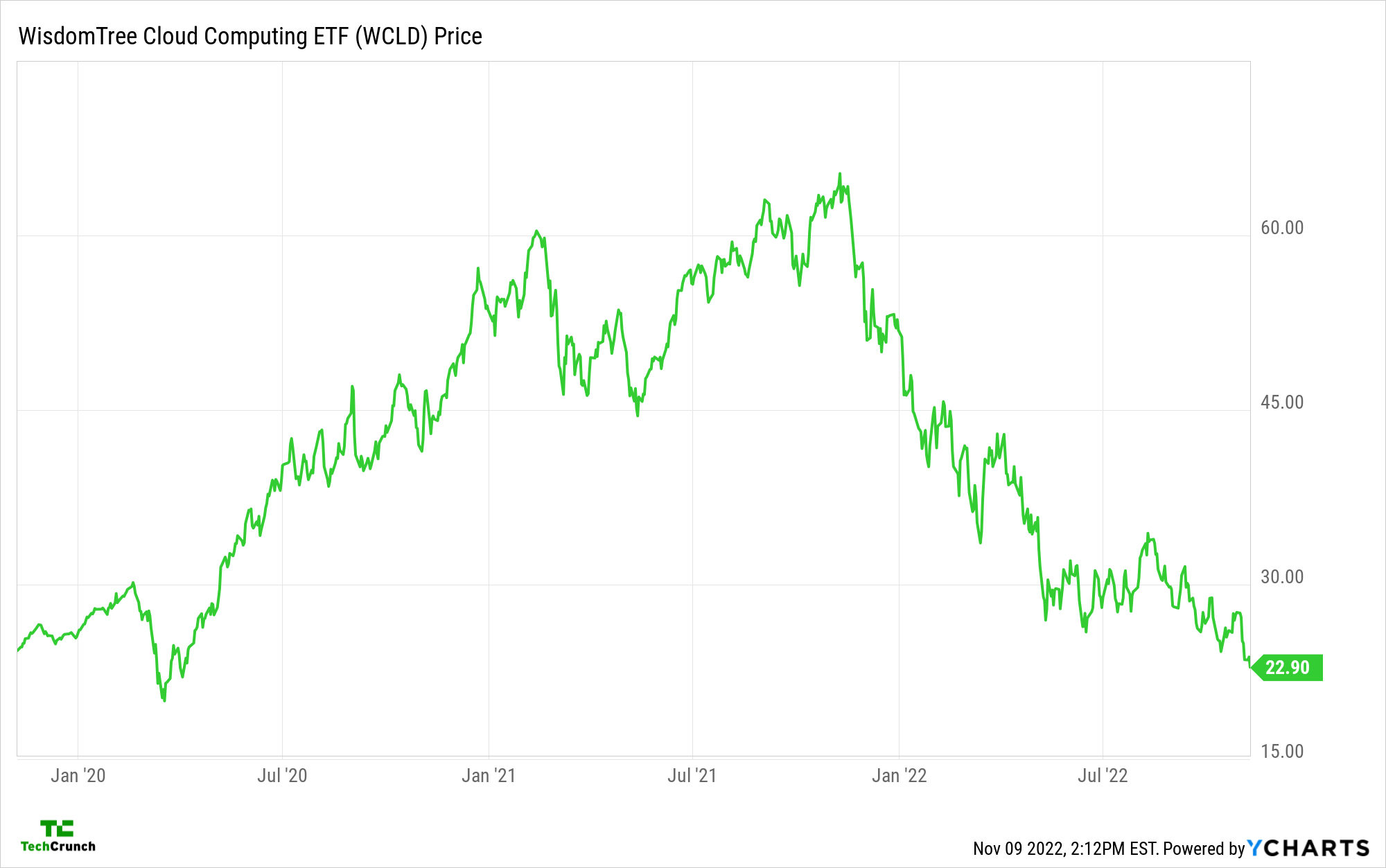

How much decline are we talking about? Here’s one way to examine the situation, the chart of the Bessemer Cloud Index:

Image Credits: YCharts

This tracks companies from Snowflake and Okta to Twilio and Gitlab. It’s the tech companies, apart from the Big Five, that you think about when you consider the value of tech stocks. It’s down by a bit more than 63% from its all-time highs. That’s bad.

But it’s actually worse than just that numerical collapse. Sure, valuations are down, but the companies underlying the selloff have been growing in the intervening year. So, prices are down and companies’ revenues are up. This is why we have seen revenue multiples compress even more than prices; the incremental value from revenue growth has been more than halved.

This is the real reason why everyone wants to invest in efficient growth now. Investing in expensive growth simply doesn’t make sense anymore. It just takes too much capital to grow revenue without a tailwind to make the math work.

As Jamin Ball wrote last Friday, the decline in the value of tech revenue continues to dip as rates rise. With more rate hikes on the horizon, the bad news could keep piling up:

Really, what would the bottom be for software valuations? Given that no one thought we would get this far, I am loath to say that we’ve hit it. There could be even lower figures coming. So much so that when we asked the other day if revenue multiples were really that useful, we weren’t messing around just to be rude. Instead, the entire edifice of how tech companies were valued for years — revenue multiples — may be proven wrong to the point of derision.

We’ve covered most of this before, but it’s worth sitting back and staring, yet again, at a new 52-week low for the Bessemer basket. I mean holy shit.