In an expected move, European music streaming company Deezer announced plans yesterday to go public via a French SPAC.

The deal values the company at a pre-money equity valuation of €1.05 billion and at €1.08 billion in enterprise value terms. Notably, those prices are similar to those at which Deezer last raised known external capital, a €160 million round in 2018 at a valuation of €1.0 billion on a post-money basis.

Naturally, with Spotify battling Apple Music for global music streaming ascendancy, and rivals Amazon, YouTube, and others competing for market share, you might have forgotten about Deezer, especially if you are not located in Europe. Still, the deal is happening, and that means we’ve been given a sheaf of information about the company.

The Exchange procured the company’s release and investor presentation. Let’s parse the data and see what the economics of a smaller music streaming business look like today.

Inside the Deezer SPAC

Starting with some top-level numbers, Deezer had 9.6 million subscribers at the end of 2021, leading to it calling itself the “#2 independent music platform globally.” Fair enough; that’s more subscribers than I would have guessed. The company generated €400 million in 2021 revenue.

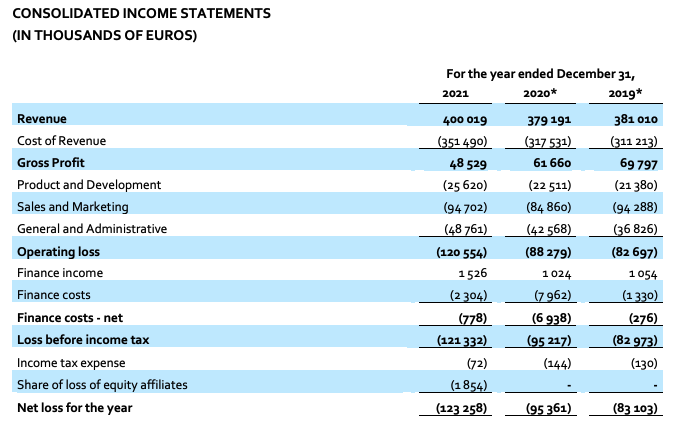

Here are the company’s core financials, via a release:

Image Credits: Deezer release

A few things jump out at once, including slow revenue growth in 2021 and negative historical growth in 2020. The company has also posted decreasing gross profit results — and falling gross margins — in recent years. Those declines are contrasted against rising sales and marketing costs, leaving the company with stiff — and growing — deficits.

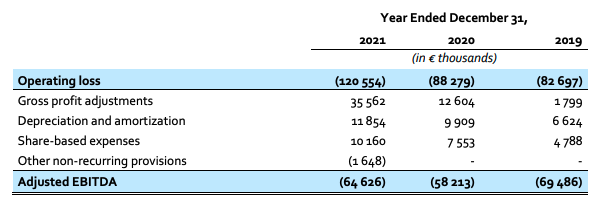

Even if we allow Deezer to dramatically tweak its profit numbers through the adjusted EBITDA moniker — more here — the results are still a bit blah:

Image Credits: Deezer release

Looking ahead, Deezer said in a release that it has “the ambition to achieve €1 billion revenue by 2025.” Again, fair enough. So, really, how good of a shot does the company have at growing into those numbers in the timespan listed?

How will Deezer grow?

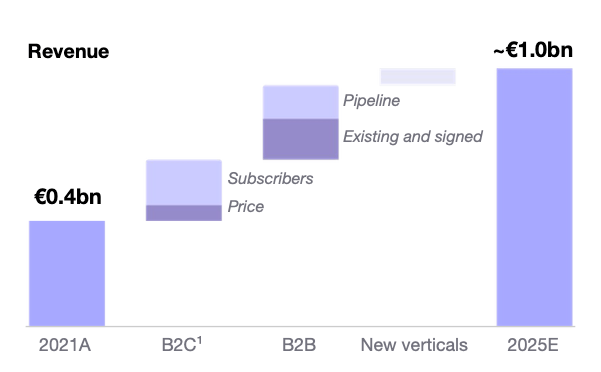

As with all SPAC decks, the Deezer presentation is a hoot. Observe the following slide excerpt:

Image Credits: Deezer SPAC presentation

Focusing on large markets makes sense and partnerships could prove accretive, but the latter two bits are a little fun when we compare them to the moniker “new strategy.” It’s a new strategy at Deezer to pursue operational excellence as a method of delivering more lifetime value? Groundbreaking. Its executive team should teach a business school class.

Snark aside, the large market and B2B push are in fact related. Deezer has existing business partnerships in France (29% market share) and Brazil (17% market share). And the company has landed deals in Germany, a market where it currently has 1% market share. Its partnerships with RTL (a German television company) and Debitel (a German mobile telecom company) could provide a lift in Deezer’s growth rate by helping it drive new subscribers.

Deezer anticipates roughly half its revenue growth to come from such B2B partnerships:

Image Credits: Deezer SPAC presentation

How reasonable is that expectation? It feels a little aggressive. Observe the following table from the company, detailing its subscriber mix over time, focusing in particular on the B2B category:

Image Credits: Deezer release

The company has managed aggregate growth in subscriber numbers, but its B2B category has proved lackluster of late. If investors decide to buy shares of Deezer when it combines, they will be effectively betting that it can rapidly scale its partnership-driven subscriber numbers.

Recent growth

Looking at 2021 numbers in mid-April 2022 feels somewhat dated, so let’s scare up the company’s latest figures:

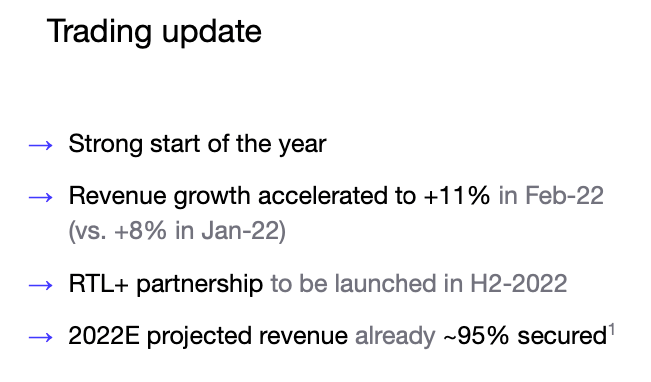

Image Credits: Deezer SPAC presentation

Deezer grew 6% in 2021 and expects 14% growth in 2022. It anticipates scaling that figure to 24% in 2023. So not only does the company expect to boost its growth rate this year, it anticipates adding another 10 percentage points to the figure the year after, reaching a growth pace some 71% faster than it expects to manage this year.

That the company’s growth accelerated from 8% in January to 11% in February is good, if modest. And while a few such data points is hardly a trend, the ability to demonstrate some expansion lends credibility to the idea that the company has acceleration in the tank.

As far as SPACs go, Deezer’s presentation is not super wild. It’s aggressive and rosy, but not insane. It’s no multibillion-dollar EV company with no production, for example. Questions remain, including the company’s gross margin erosion and how its new partnerships will truly unlock the German market. It’s going to be an uphill battle for Deezer, in other words.

More capital will help. And we’ve been asking for more unicorn IPOs, yeah? Well, here’s something close. More when it combines.